"Secrets to Saving Money in Australia" Free Newsletter - May 2010

This issue includes:-

- Sad Sally, Happy Hanna: Here's One I Made Earlier

- June is Double Dinner Challenge!

- This Month's Competition: Best Double Dinners

- Before and After Competition Winners

- NEW! Hidden Gems Directory

- Best of the Forum: Cook Once, Eat Twice

- Best of the Vault: Delightful Double Dinners

- Savvy Cook Showcase: 'Sizzler' Style Cheesy Toast

- Penny's Blog: New Tricks

- Homeopathy Corner: The Big C

- From Last Month: Spendaholic Husband

- This Month's Help Request: Coping as a Carer

- Savings Story: $14,000 a Year Savings

Hello,

How are you going? Life in the Lippey household has been charging ahead. Elora's hair has grown long enough for a hair fountain (top knot)! Here she is, waving hello to everyone. I love it when the littlies learn new tricks!

As you can see below, she has also mastered the didgeridoo. OK, so it's not exactly a didgeridoo. It is a Post Pak tube and she is trying to bite it. The real reason it is in her mouth is she thinks it is a giant teething rusk.

If you get the impression from these photos that sometimes I get a little lost in baby land and chase my kids around the house with a camera, you'd be right! I can't help myself, it's so much fun. I love taking photos of the kiddies because I am so proud of them. I'm also proud of the $21 Challenge book and the way we all built it together. When we get letters like these ones, be proud, because they are thanking you for helping us build it together.

"I just wanted to say a very big 'thank you' for the $21 Challenge concept and book.

"After a bit of overspending this month and an unexpected dental bill, I literally had around $21 left in the bank at the end of last week. I worked through the book on Saturday. It took me a few hours to do the inventory of my fridge, freezer, pantry and garden - I didn't realise just how much food I had in the house. (I also found a few 'science experiments' lurking in the fridge and things well past their use by dates!)

"I set my goal to feed my family (myself and my cat!) at $21 max - for all breakfasts, lunches and dinners for a week. I thought, if a family of four humans can do it, surely a family of one human and one feline could do it too!

"Then I worked out my menu plan. I discovered that all I needed to buy to get us through this week was a packet of oats, one carrot, one cucumber, three bananas and a few green beans. Total expenditure on food this week? A measly $6.64! On top of that, I already have four dinners on next week's menu plan using items I already have in the house - so I shan't be spending much money next week either!

"The whole exercise also made me think about what other household commodities I actually NEEDED to buy this week. Answer? Just a packet of toilet rolls, cost $3.31. So my total household expenditure for this week is under $10! I'm also going to review all my other household expenditure, using the Vault of course, and see what other savings I can make.

"I know it's only the cat and me, but $6.64 is a HUGE saving over my usual $70-$80 per week on food alone! If I can do that even once a month, I can save nearly $1000 in a year, and as a full time student living on Austudy and some savings, every dollar counts. Once again, I can't thank you enough for inventing the $21 Challenge!" (Sandy Jennings)

"I finally decided to bite the bullet and buy your book. I read it and soon realised that I had roast beef and a bag of lettuce from last weekend and mountain bread from two weeks ago sitting in the fridge. Some of the lettuce was used last night for salad to accompany my home made quiche, then for today's lunch I made beef and salad toasted wraps. The rather brown bananas I had been wishing would be eaten got turned into banana bread. It all seems so simple, why didn't I think of it before? Thank you so much for turning the light bulb on for me and opening my eyes to the food I was just throwing away. I can't wait to put my newly acquired knowledge to the test when I do the food shopping this week!" (Tanya McSwan)

"We completed our first ever $21 Challenge. My first trip to the shops came to less than $14. My husband could not believe it! Even with buying the A2 milk my toddler has to drink and gluten free bread for my hubby, our grand total came to just $30. Sure beats the $300 that I was spending! The great thing is that I have enough frozen food to last me a couple more Challenges and have barely touched the pantry! We were getting very low in money, and because of this Challenge, we have been able to save more money this fortnight." (Rebecca Sennet)

"I bought a copy of The $21 Challenge and gave it a go. We succeeded in spending only $19.85 for the week and I could not hold back my excitement! I shared some of the tips with my colleagues at work and all of a sudden I had an excited audience. One colleague in particular has now taken on board some of the tips and uses a shopping list when supermarket shopping. She writes down only what she needs to purchase to create a meal - and nothing else. Not only has the $21 Challenge helped my family change its thinking when shopping, I have also helped a colleague. A terrific feeling!" (Tracie)

All the best,

Fiona Lippey

P.S.: Secret Society of Simple Savers

It wasn't on purpose, it was never meant to happen, but it has. We have become a Secret Society of Simple Savers. Think about it - do any of your friends know you are a Simple Saver? Do you know if any of your friends are Simple Savers? Are you and your friends on the same journey but neither of you know about it, because at the last family get together you never thought to ask the question, 'Are you a Simple Saver?'. Well, no more - Facebook has come to our rescue. (I knew there had to be some purpose for that thing!) Simple Savings now has its own Facebook page, and by clicking on the 'like' button you will be starting a conversation with your friends and family to find out if they are Secret Simple Savers too. And, if you are really lucky you might even find someone to share your Double Dinners with! (We will tell you more about those in a minute.)

P.P.S: Check out this brilliant full page feature on page 10 of the Melbourne City Newspaper! With an informative article on the $21 Challenge, Fiona's Eight Steps to Happiness and a fantastic story from one of our members, Sharyn Polatos, what more could we possibly ask for? Click here and turn to page 10 for the full story. Thanks MCN!

1. Sad Sally, Happy Hanna: Here's One I Made Earlier

'Brr, it's freezing!' shivered Hanna. 'I think I'll make a nice stew for dinner tonight!' 'Hmph - I've got a good mind to go on strike and let my ungrateful lot sort their own dinner out!' Sally scowled. 'It's the same every night. Pete gets home from work and flops down in his comfy chair. He gets to watch the news in peace for an hour and nobody is allowed to interrupt him.' 'Sounds familiar!' chuckled Hanna.

'Meanwhile I'm out in the kitchen cooking dinner by myself. The only time anyone talks to me is when they want something. Then they all scoff their dinner and disappear quickly before they get asked to help clean up. I've had enough! Nobody appreciates me. I just want a night off,' Sally fumed.

'I know what you mean. Then let's have a night off! Heck, let's have a week off!' grinned Hanna. 'Now there's a lovely thought - in my dreams!' grumbled Sally. 'No really, Sal - we could do it! How about this week we cook twice as much of everything and freeze half of it. Then next week we could have the whole week off!' 'Wow, no cooking for a week?' Sally smiled dreamily at the thought. 'That sounds like heaven! But - how, Hanna? How on earth would that work?'

2. June is Double Dinner Challenge!

Sally's cartoon dream is funny, but not very practical. The best way to get a week off cooking is to make a big batch of frozen meals. Pulling a nutritious, home-made dinner out of the freezer is heaven. When life is hectic I love being able to just grab a container of food, nuke it, throw in some herbs, stir, nuke it some more and serve. A true no brainer meal for the days when I have no brain (which is surprisingly often...).

My friend Marge taught me about true no brainer meals. When her husband had cancer, she would cook him nutritious meals in bulk and freeze them in containers. Then any time he felt like eating, he could just pull the food out of the freezer, nuke and eat, no matter what time of the day or night it was. (You may already have 'met' Marge in our Pumpkin and Vegetable Soup YouTube video. She also features on page 126 of the $21 Challenge book, in the recipe for Marge's Tomato Soup. Both recipes are the same soups she made for her husband. He was a lucky man.)

Marge's husband has since sadly passed away but she still cooks in bulk and takes her frozen meals visiting. If any of her friends are ill, she takes them a couple of meals to pop in their freezer. I think this is a fantastic idea and a lovely gesture so you know what? I've decided I am going to follow her lead. From now on, whenever a friend is sick, swamped by small children or life in general, I'm going to turn up with a big pile of 'no brainer' freezer meals. This way, the people I care about can have a couple of nights off too.

This month I want you to spoil yourself as well! By making some no brainer meals you can enjoy not just a night off, but a whole WEEK off cooking. All you have to do is cook double quantities for seven nights. Then you get the whole next week off! It doesn't get much simpler than that.

This is how we do it:

- Choose some one pot recipes.

- Multiply the ingredients by two.

- Don't add any of the herbs or spices the recipe asks for yet (herbs taste strange when you freeze them. Garlic in a jar, ginger, curry paste and onion are OK but not dried herbs or fresh garlic).

- Cook the meal in a big pot.

- Scoop out half the mixture into containers with lids and leave on bench to cool.

- Add half of the herbs into the pot and put the other half in a safe place for later.

- Enjoy your freshly cooked meal!

Now, when you are clearing up after dinner, put the other container of food in the freezer. Then, next time you want a 'no brainer' night, simply grab your containers from the freezer, defrost in a bowl in the microwave, grab those herbs you saved from before and add them, stir, heat and serve. How easy is that!

I love my nights off cooking, it is my absolute favourite cheat. To make sure you have absolutely no excuses for giving it a go, here are two yummy recipes to get you started.

Fiona's Iron Curry

Makes two meals for four adults.

This energy boosting dish is for those 'lacklustre' days - you know the ones where you feel worn out, your hair looks limp, bags under your eyes and your skin is just blah? When that happens, I'm usually low in iron. This dish came from me trying to jam as much iron and nutrients into my family in one meal as possible.

Spinach is high in iron, meat is high in iron and tomato helps the body absorb iron. So this is a 'pick you up, give you energy, make you look good' meal. Matt calls it 'Iron Curry' and I think it's a pretty fitting name. As long as you don't tell your family it's healthy, they'll love it.

- 1 onion

- 2 bunches of silverbeet

- 2 zucchini

- 2 cups brown rice

- Dash of oil

- ½ tsp powder ginger (can be fresh, whatever you have)

- 1 tsp garlic

- 4 tbsp curry paste (any type, your choice)

- 1 kg minced meat

- 2 cups water

- 2 400g tins tomatoes

- 1/3 cup of peanut butter

Start by cooking your brown rice in the microwave. Put your two cups of brown rice in a microwave rice cooker with four cups of water on high for 18 minutes, then forget about it for a while.

Wash the silverbeet and get rid of the stem, then loosely chop the silverbeet and zucchini (the smaller you chop them the faster they will cook). Put a large pot on the stove to heat up and put in the oil, ginger, garlic, onion and curry paste. Stir them for a minute and throw in the meat, stirring until it's brown all over. Add your water, zucchini, peanut butter and tinned tomatoes. Bring everything to the boil, then add the spinach. Cover with a lid and simmer for 20 minutes. When it is done blend the lot in the pot with your stick blender. Now you can grab your cooked rice out of the microwave and divide half the rice and the curry mixture into freezer containers. Enjoy the freshly cooked other half for dinner!

IMPORTANT: Freeze the rice and Iron Curry in separate containers so you can defrost them without the rice consuming all the liquid.

Apricot Vegetables (with a dash of chicken!)

Makes two meals for four adults.

Once upon a time this was a recipe for Apricot Chicken but I jammed so many vegetables in it I thought I should really change the name!

- 2 cups brown rice

- Dash of oil

- 3 onions

- 840g tin apricot nectar

- 1 kilo chicken thighs

- 5 carrots

- ½ bunch of celery

- 500g beans

- 125g cheese

- 4 tbsp cornflour

- Nutmeg

Put the brown rice in a rice cooker or large bowl with four cups of water and place in the microwave on high for 18 minutes. Then forget about it until you need to serve.

Dice everything - onion, cheese, carrots, celery and beans. Next dice the chicken thighs. Warm up a large (8 litre +) cooking pot, splash some oil in the bottom, then throw in your chopped onion and cook gently until soft. (If you want to save time you can do this whilst cutting up your chicken.) Pour in your tin of apricot nectar and blend with a stick mixer. Bring to the boil and add the chicken, carrot, cheese and celery. Bring back to the boil and simmer for ten minutes. Add your beans and simmer for a further two minutes. Mix your cornflour with enough water to make a paste, then pour into the pot and stir well to thicken. Grab your cooked rice out of the microwave. Divide half of the rice and chicken and vegetable mixture into freezer containers. Enjoy the other half for your dinner, served with a sprinkling of nutmeg.

Now it is your turn! What are YOU going to cook? How are you going to do it? Just as importantly, how much fun are you going to have? To reward you and support you, we are having a best blog and best recipe competition. I'm looking forward to reading how you go, not to mention trying out some of your fabulous recipes!

3. This Month's Competition: Best Double Dinners

This month we have TWO prizes of $200 to give away! As you will see in this newsletter, keeping a diary or blog of your challenges is a fantastic way to stay motivated and keep on track. So this month we are encouraging everyone to blog your Double Dinner challenge. Share your experiences and your recipes with us and you could win a cash prize! The best Double Dinner recipe and the best blog will each be awarded $200.

If you've never cooked in large quantities before, don't be scared to give it a go! It really couldn't be easier. We have already given you two yummy recipes to get started and there are tons more recipes for bulk cooking and freezing in the Savings Vault and Member Downloads area. Think about the dishes your family likes to eat. What are your favourite dinners? What are your easiest recipes? Would they freeze well? Don't be scared to ask if there is anything you are not sure about - our team is here to help you or you can always find a helpful answer in the Forum. The only real essentials are a stash of freezable containers (empty ice cream or takeaway containers work just as well as anything else) and a big pot.

How to enter

To enter the recipe competition, go to this page and submit your recipe. We will choose the best tasty, funny, money saving recipe. We shouldn't, but I have to confess the recipe judges are easily influenced by funny/informative/funky photos!

To enter the blog competition. Blog your week on your usual blog or in the Vault and when it is done, email us here so we can come and read it.

All entries must be to us by the 25th June so we have time to choose the winners and put their fantastic results in next month's newsletter.

So what are you waiting for? Get cooking - and get blogging! Good luck and have fun!

4. Before and After Competition Winners!

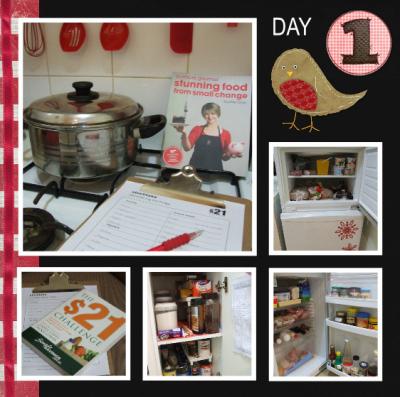

Last month we asked to take a peek inside your pantry - before and after a $21 Challenge! The most inspiring entry came from Sarah PN, who also blogged her $21 Challenge as she went. Sarah has won a cash prize of $200. Congratulations!

Here is a shortened version of Sarah's winning entry, featuring some mouthwatering photos of some of the meals she enjoyed from the $21 Challenge book. The full version, including recipes and Sarah's menu plan is here. As you can see, she has done an amazing job!

Today marks the start of my $21 Challenge! I filled in my spending target for the week as well as my reasons for wanting to do the Challenge, according to the instructions in the $21 Challenge book:

Our $21 Challenge Target

- Who are your teammates? Myself and my dear husband, Simon.

- How little are we going to spend on food this week? $21 or less.

- What will that sum include? All food.

- How much will we save by sticking to that target? Approx $50.

- What are we going to do with our savings? Put them towards the mortgage.

My Top 5 Reasons to Take the $21 Challenge

- It will give me more control

- It will make me feel good

- It will help me to be healthier

- It will give me security

- It will help me get ahead

Next I downloaded the stocktake lists from www.21dollarchallenge.com/tools and set off to the kitchen, clipboard in hand, to delve into the freezer, declutter the fridge, and explore the pantry! We pulled everything out, covered the shelves with red non-slip matting, and put it all back. I'm quite happy with how it turned out and feel the Challenge is off to a good start!

So far all we need to buy is:

- Pita bread $2.09

- Cous cous $2.25

- Coconut $1.85

- Milk $2.09

- Rice $2.79

- Cream cheese $1.89

Total bill for the week: $12.96!

Having not gotten myself organised in time to have breakfast this morning, I craved anything and everything I saw people eating at the train station. Those potato cakes smelled so good! I reminded myself: not only will doing the $21 Challenge save me money, but it will make me healthier too. I will make sure to get up on time tomorrow, have a decent breakfast, and not be tempted by fatty potato cakes!

We have got through another day without spending any money on food! After a long day at work, and being 'cheap night' at the movies, hubby and I decided to go out for the evening, but not break our Challenge. So, we made sure to eat before we went - we had one of our frozen bonus meals that was sitting in the freezer and made pineapple mousse to enjoy for dessert when we got home.

It was only after we got back from the movies that I realised the front of my black-and-white dress was splattered with pineapple mousse (from the blending). Eek! How embarrassing... hopefully it blended in?!

Today turned out rather differently than expected. We ended up meeting a friend for a farewell dinner at Ikea! We figured out that we could afford one meal out as part of our $21 Challenge - provided we chose items that were on the specials list. Chicken schnitzels with chips, lemon and condiments were just $3.95, as was the organic pasta or the sausages and mashed potato. At $7.90 total for the two of us, we are still under budget at $20.86!

Blueberry pancakes were on today's menu but I didn't end up making them after all. With so many leftover desserts such as fruit jelly, Budget Bix slice and mango mousse I thought we should eat some of that up instead. The roasted vegetable salad was delicious though! Just goes to show what an awesome book 'Stunning Food from Small Change' by Sophie Gray is. I must also say that this week's lunches have been the best in ages! I'm not missing my bought lunches anymore.

What can you do with one and a half carrots? You can make carrot soup! By this stage of our Challenge, we had only one and a half carrots and no onions left! So it was time to stretch my stretching powers a little. Here's my modified version of the Carrot Soup recipe on p.197 of The $21 Challenge :

Sarah's 1-and-a-1/2 Carrot Soup

(aka. Spicy Cream of Carrot Soup)

serves 2

1 1/2 carrots (no matter how small), sliced and then chopped into semi-circles

1 tbsp of butter or margarine spread

Salt to taste

4 cloves of garlic (or 1 small onion), chopped finely

1 cup of stock (any kind - vegetable is best, but I only had beef)

1 cup of milk (fresh or from powder)

1 tsp ground turmeric

paprika to taste

Garnish (optional):

Sweet chilli sauce

2 tbsp cream cheese OR 2 tbsp cream

Thinly sliced capsicum to garnish (optional)

- Boil the carrots until soft, then mash in the saucepan with butter and salt.

- Add all other ingredients and bring to the boil, then allow to simmer until fragrant.

- Serve hot, with a swirl of sweet chilli sauce and a dollop of cream cheese or cream as preferred.

After a draining weekend visiting my seriously ill grandfather, Simon offered to take me out to dinner and a movie, but we decided to wait until the end of the Challenge and stay in. We watched DVDs and had a 'healthy' but deliciously junk-foody version of nachos!

Spicy Hot Nacho Dip recipe here: www.recipezaar.com/recipe/spicey-hot-nacho-dip-415076

My FINAL DAY of the $21 Challenge - and at last we had a day that went to plan! I made the Quick Microwave Apple Pudding this evening, a recipe I had chosen especially for Simon, as he loves everything apple. Our tiny kitchen was quickly filled with the delicious scent of hot apple and sugary cinnamon. It is such a great recipe, so simple, and yet so comforting and delicious on a cold almost-winter's night. Eventually, the smell became so delicious, I had to call hubby out to the kitchen to share it with me, and we both sat there watching the pudding cook until it was golden and ready. What a great end to the $21 Challenge!

The big question of course is, how does our pantry, fridge, and freezer look now?

Here is the final state of our kitchen after our $21 Challenge. I'm glad that we got to use up some of the items that had been lingering in our pantry though, and use up all of the fresh fruit and veg that may otherwise have gone off and been wasted. It's not quite an 'Old Mother Hubbard' situation, but I am looking forward to grocery shopping!

Congratulations on a fantastic effort Sarah! Thank you to everyone who entered. Four runner up prizes of $50 have also been awarded to: Jenny Blair, Siboney Duff, Samantha Elley and Denise Jury

Well done!

If you would like to order a copy of The $21 Challenge

you can order it directly from us by

clicking this link or go to your local book store.

5. NEW! Hidden Gems Directory

Thank you for sharing your favourite Hidden Gems with us! As our directory grows it is going to become a fantastic place to find the best bargains on all sorts of things in your region. Each month in our newsletter we are going to focus on a different type of Hidden Gem. This month, we want to know where all the best hairdressers are hiding!

When we first moved to Buderim there were two things I had real trouble finding. A good butcher and a good hairdresser. You see, many years ago my mum spoiled me. She took me to a really expensive salon in the middle of Sydney and they did such a good job that everyone I met for the next couple of weeks said, 'Wow! Have you lost weight?' I hadn't lost weight, it was just a great haircut! So for years since I have searched for a hairdresser who can cut hair as beautifully as that salon in Sydney. Finally, after sampling eleven different hairdressers, I found a reasonably priced hair cutting genius!

Here is my Hidden Gem this month. Let me introduce my wonderful hairdresser Christine!

Store name: Christine

Address: Anzac St, Eudlo

Phone number: 07 5478 8485

About the store: Christine is a fantastic and well priced cutter. She is also a lovely lady and great with kids, which is a nice bonus. She is no fuss and has a great eye for what looks good on people. In an amazing coincidence, 40 years ago Christine was apprenticed to Penny's mother in-law in NZ!

How to get a great price: There are no special tricks for getting a 'good price' hair cut with Christine. Her prices are reasonable and don't tell her, but she does such a great job I'd happily pay twice as much! It is nice knowing that after I have been to Christine people are going to say. 'Your hair looks nice.' Once after having it done, a lady at Sam's school didn't even recognise me! She had to do a double take!

If you know of a fantastic hairdresser in your area that consistently provides excellent value and service, tell us about them! Write in and share your Hidden Gems here. Vault Members; If you haven't checked out our Hidden Gems directory yet, you can take a look here.

6. Best of the Forum: Cook Once, Eat Twice!

Whether you like to cook once a month, once a fortnight or once a week here are some great threads from the Savings Forum sharing recipes and tips on how to freeze yummy, ready to eat meals in a jiffy!

Recipe file - OAMC and freezer recipes plus more

This is a recipe file not to miss! Belinda shares her best Once a Month Cooking recipes with an easy download for you to keep. Thanks Belinda!

read more...

Basic crockpot mince mixture...7 meals from 2 kg!

Mimi has a wonderful way to stretch mince into seven meals! Simply make a big batch and freeze and it's ready to use in seven different and delicious ways.

read more...

I hate cooking dinner (seriously hate it)

Hate cooking? Then this is the thread for you. You are not alone and there are great ways you can cook double without noticing so you don't have to cook every night. Give it a go!

read more...

OAMC - I have to brag and ask for ideas : )

Need to find some inspiration for a cooking session? Learn from our savvy members how they prepare and manage a once a month cook up.

read more...

7. Best of the Vault: Delightful Double Dinners

Cooking extra meals in advance is a fantastic way to avoid takeaway. And it just goes to show that you can include your friends and family in your double dinner plans and swap meals as well!

Don't double all the ingredients

I always cook twice the amount so that I can freeze some of the final product for consumption later. This means that I can produce muffins or similar at breakfast and lunch. To reduce the costs, I do not double expensive ingredients such as dried apricots or blueberries. Sometimes I leave out expensive ingredients such as pine nuts, and sometimes I use a cheaper substitute.

Contributed by: Annabel Brinkworth

Swap cooked meals with friends

My friends and I have very busy lifestyles and often save time and money by doing the following:

We all have a favourite recipe that can be frozen. We buy enough ingredients of our individual recipes for eight meal-sized serves (four couples), and cook up a giant batch. We then freeze the meals in plastic containers and swap them; each couple now has four different frozen meals. This means that we don't have to cook for four nights!

It's a fantastic way of saving time and, because we can buy in bulk, it's also cheaper than making a batch for two. I make a vegetable-and-beef stew in my pressure cooker for about $2.50 per serve!

Sometimes if the weather is a little miserable we gather together to make the meals, and have a ball just being together. This is cheap entertainment!

Contributed by: Wendy McDermott

Cook and freeze

I buy mince in bulk when it is on special and cook up a big pot of spaghetti sauce, which I freeze in batches.

This sauce is not only good for quick spaghetti bolognaise, but it can also be used for ravioli, lasagne, mince on toast - the list is endless. I find that making the original batch without a lot of herbs and spices works best, as I can always add different flavours when it's time to use the sauce.

Contributed by: Margret McPharlin

Cooking up extra batches saves fuss later

When you are cooking make up 1-2 kg batches, say of casseroles, soups or bolognaise sauce. It will only take a little longer to cook than a one off meal but you will have plenty to freeze for those times when you're too tired or no time to actually cook but want a meal fast. When baking, make a day of it and do six or more and freeze for later.

If you're doing a sauce to go with pasta, cook extra pasta each time you have it and freeze in meal size lots. This will reheat in a pot of water in under two minutes and you already have the sauce made. Simply toss the sauce into the nuke machine on the defrost setting and in around 15 minutes you have a great home cooked meal with a minimum of fuss. Great for those with physical limitations such as arthritis, fibromyalgia, M.S., chronic fatigue and so on. You know who you are. You know what it's like, you're beat but starving.

This takes the load off, saves you money with power and your own energy!

Contributed by: Leonie Cechini

Avoiding takeaway

I always make dinner on a Sunday night and make lunch and dinner for much of the rest of the week. I have commitments two nights of the week in the early evening that mean I must eat on the run or eat out. This means that I average six meals a week that I can't cook easily so have to think laterally to overcome ... so on Sunday night I make dinner and also cook another meal. This week for example I made a chicken curry.

- Chicken tenderloins: $6.00 for 500g

- Tandoori paste: $3.00 for 1/2 jar

- Coconut cream: $2.00 for 300ml tin

- Frozen vegies: $2.00 for 500g bag

- Rice: $1.00 for two cups

Fry the paste for a few seconds then add the chicken. Stir to coat then add the coconut cream and 1/2 can of water, along with the vegies. Simmer gently until the chicken is done. Cook the rice and divide it up!

This is making me four meals for $14. To make six meals a week that would be $21 as compared to $60 to eat out!

At $3.50 a meal, I'm saving around $6.00 a meal. It's also healthier for me so I'm saving money on my health costs as well. Over a week that's $36 in savings or $1872, which is an annual trip overseas!

Contributed by: Emma Skelton

Two meals in one saves time and money on groceries

I save time and money on my grocery bill by planning how I will create a second meal out of the leftovers of everything I cook. When I go shopping, I also buy ingredients for the second meal if I don't already have them. For example:

- First night: Roast chicken

- Second night: Chicken fried rice

- First night: Corn meat

- Second night: Corn meat fritters

- First night: Pasta bake

- Second night: Shepherd's pie

- First night: Lamb chops

- Second night: Lamb casserole with vegies

This method has been successful for us by making it quicker and cheaper to cook meals.

Contributed by: Laurent Menigoz

Here are some other recipes available to Vault members:

$13 mince mix makes base for 7 meals Contributed by: Mimi

'Borrowed' pizza Contributed by: Onwards and Upwards

A large pot of food savings Contributed by: Margaret Rendina

A saucy side dish idea Contributed by: Anna Francis

Bacon recipe to feed family for $1.60 Contributed by: Michelle Zappulla

Brown Rice and Tuna Slice Contributed by: Shane O'Donnell

Cheap and versatile meal base Contributed by: Hugh Johnson

Cheat's Lasagne Contributed by: Sharon Bohlsen

Chef's own pasta Contributed by: Leigh B.

Chicken Tetrazzini Contributed by: K

Favourite freezer cooking recipes Contributed by: Melanie Lindner

Freeze cooked rice and pasta for quick meals Contributed by: Marilyn L.

Home-made sausage rolls Contributed by: Trace babes

How I fed a crowd for very little Contributed by: Janet C

Low cost tomato soup Contributed by: Irene Jones

Make your own chicken nuggets Contributed by: Ezri

Pie surprise Contributed by: miss A

Prepare your own frozen roast dinners Contributed by: Pauline Seretis

Rice on ice Contributed by: Lorna Reynolds

Savoury Stew for tight budgets Contributed by: Clarice Boland

Super soupy chicken casserole Contributed by: MissMimi79

Taco mince without the expensive kits Contributed by: Michelle Zappulla

Tomato and Vegetable Soup Contributed by: Sharon Bohlsen

Tortilla 'takeaways' from your freezer Contributed by: Amy Diffey

Vegetable lasagna Contributed by: Shane O'Donnell

8. Savvy Cook Showcase: 'Sizzler' Style Cheesy Toast

This month's winner is Mimi for her fantastic version of a much loved old favourite. Who remembers the delicious, golden Cheesy Toast that you could only get from Sizzler restaurants? Clever Mimi has found a way to replicate this yummy classic in the comfort of her own kitchen, to make an affordable treat her family can enjoy any time. Another bonus of this simple recipe is that it is VERY filling. A perfect, low-cost choice for feeding hungry guests! Mimi wins $100 cash prize for her contribution. Well done!

'Sizzler' Style Cheesy Toast

Mimi says "My kids love this for a quick and easy lunch, snack or accompaniment to our gourmet 'better than tinned' spaghetti.

"The kids love to make the cheesy spread, and flip the toast, and it's always a treat consumed to many groans of 'yummmmm!'

"You can use any sort of bread or bread rolls, but make them thick slices for authenticity!

"This saves us so much money, because we realised we only really go to Sizzler for the Cheese Toast! It's also a great way to use up ends of home-made bread and stale rolls of any kind."

Cooking Time: 2 minutes

Preparation Time: 10 minutes

Serves: 6

Cost: $3.00

Ingredients:

- 12 slices thickly sliced bread, or 6 halved rolls of any shape or size. Halved hamburger rolls are perfect. For authentic Sizzler flavour, only use white bread or rolls.

- 250g butter, dairy spread or margarine, softened

- 1/2 cup finely grated fresh or dried Parmesan cheese (the dried Parmesan will have a stronger flavour. You can find it in the pasta aisle of the supermarket)

Equipment:

- Frypan

- Grill, or griddle pan (one of those ones that leaves a 'stripe' on your food when cooked)

- Spatula

Method:

Mix the softened butter, margarine or dairy spread with the Parmesan cheese.

Heat the grill or griddle pan and 'toast' your halved rolls or bread until lightly browned.

Spread the bread or halved rolls thickly on the UNCOOKED side, and set aside. Allow the spread to melt a little into the surface of the bread.

Heat the frypan over the highest hotplate setting, and quickly 'sizzle' your toast, spread side down. You only want to melt the spread and crisp the surface, so 20-30 seconds should do it! Press on the bread with a spatula to get the spread all hot and super crispy.

Serve immediately to happy faces:

Notes:

This is a quick, fun holiday or weekend meal, and can be turned into a gourmet meal with the addition of side salads and deli meats, or your favourite pasta dish.

Best made fresh as required.

Spread keeps well for several weeks in the refrigerator.

Keep sending in your yummy recipes for the chance to win a monthly cash prize! Send them in to us here.

9. Penny's Blog: New Tricks

May 26, 2010

It's amazing what you can do when you try! Take the last week or two for example. Liam has learned that he can live very easily without Facebook now it has been blocked from our computer. Ali has learned that if you hold on for long enough you can bring down an 85kg chap on the rugby field, even if you're only 35kg yourself. And I've learned that being a school teacher is very hard work but can be hugely rewarding and a lot of fun! Yes, for the past three weeks I have had the pleasure of teaching a life skills class to the Year 12 students at the local college. The aim? To teach them smart money habits the Simple Savings way at 16, so that when they leave home they don't end up like I did, broke and clueless at 32. Easy peasy! Or so I thought...

'Now - you're going to need to talk for an hour at a time, can you do that?' asked the Head of Department. 'Can I do that? Pah - you're looking at a veteran of 50 squillion Simple Savings talks lady, I can do this standing on my head!' I thought, but didn't say. As far as I was concerned I had it sussed. The first week would be based on how to be smart with your money, the second week would cover all the daft things people do to throw away their money and the third week would focus on long term goals and how to achieve your dreams the Simple Savings way. I was really looking forward to it! Unfortunately my kids were appalled at the prospect of having their mum parading around their school. 'Now for goodness' sake Mum, don't call the other kids by their names in class, otherwise they'll think 'Hey, how does she know who I am?' Liam gave me a stern warning. Ali on the other hand was more concerned with my looking the part. 'No way Mum, you can't go looking like that!' he rolled his eyes at the sight of me wearing jeans, a hooded sweater and purple baseball boots. He rifled through my wardrobe and picked out a floral blouse and suitably 'boring' shoes. 'THAT'S the sort of thing teachers wear,' he advised sagely.

I also sought the advice of 17-year-old Alex on the subject matter I had chosen for the class and whether he thought it would appeal to young people. 'Yep, that looks good,' he said. 'But are you sure you've got enough material for a whole hour's lesson?' 'Yeah, this will be heaps to go on!' I said confidently. 'Oh well, as long as you're sure,' came the reply. Sure? Of course I was!

The big day dawned and I realised I was terrified. Fortunately I had an enormous desk at the front of the class to plonk all my stuff on, so I could refer to my notes constantly without the students realising I was doing it! The lesson began and straight away I got their attention, just the way the Simple Savings website had first got mine years ago. Fiona has said to me many a time 'Teaching people to save money is easy. Making people WANT to save money is the hard part'. So I went for the tactic that I thought would appeal most to teenagers. In a nutshell, the smarter you are with your money and the more you can save, the less you have to work. You could literally see the lightbulbs going on inside their heads! Just like these teens, until I heard of Simple Savings, I had never had any reason to want to save money before. I knew I HAD to, because I was fast sending us broke - but that had always been the problem - I had never wanted to, until I read the Home Page. If you haven't read the Simple Savings Home Page for a while, go and read it, right now! You'll have to log out to see it if you're logged into the Vault but do read it. It talks about just that, how being smart with your money will enable you to work less and achieve your dreams. Sometimes it's great to just reaffirm with ourselves why we do what we do and why Simple Savings is so darn good.

Anyway, the first lesson was going along swimmingly. We discussed the 'Time is Money' equation and they were horrified to discover that one of their friends would have to work 60 hours at his part time job just to pay for the lollies he bought each week. We talked about wants vs needs when it comes to what we spend our money on and how little bits of money add up to a lot. At this stage one of the students was reprimanded by the teacher aide observing in the corner for texting in class 'I'm not!' he protested indignantly. 'I'm using the calculator function to work out how much I spend on chocolate!' We talked about how to shop around for the best price on things and before I knew it I had gone through the entire lesson plan. There was just one rather large problem. We were only 20 minutes into the lesson - we still had 40 minutes to go! What on earth was I going to fill it with? There was only one thing for it - I was going to have to reach deep into my SS brain and pull out as much information as I could. Those poor kids wouldn't have known what had hit them as I bombarded them with one thing after another, going off on one tangent to the next. By the end of the lesson I don't know who was more exhausted, them or me!

Mercifully my first class finally came to an end. I had a whole new respect for teachers and the amount of work that goes into planning an effective lesson. I had also never had such a sore throat in my life! 'That's why most teachers carry water bottles,' grinned the teacher aide. 'That was really good!' he said. 'Just one thing - you don't have to talk ALL the time. Give the kids something to do, so they can put what you're teaching them into practise. It also gives you a chance to rest your voice for a few minutes!' Bingo! Of course! Those poor kids had sat there as good as gold while I had done nothing but ramble on at them for an hour. I fully expected them not to bother coming back the following week but they must have been gluttons for punishment and from then on I made sure I was much better prepared.

By the time we got to the third lesson I was much more relaxed and really enjoying the kids' company. I learned that teenagers are a lot more switched on than we give them credit for and as we discussed their goals and dreams for the future I was pleasantly surprised. Only one student out of 23 had no idea what she wanted; the others wanted anything from their own home to their own veterinary clinic, a trip around Europe and in one girl's case, 'a Dodge Viper and a trip around the world!' We had heaps of fun drawing up a budget using the Bill Payment System. First we went through all the junk mailers, circling all the things they would like to buy once they left home and were earning their own money. I loved listening to all the discussions, especially how they were now seeing all the sales spiel for what it really was! Then we had a go at filling in the Bill Payment System using the average monthly wage and trying to make ends meet as we paid the average monthly bills, based on national statistics. We were all shocked to see just how little was left! It really opened their eyes and made them see how important it was to pay for the essentials first, because then they would know that there was no way they would be able to afford a widescreen television, even if it was 12 months interest free. It was a great way to show that living within your means is possible but you have to use your money the right way round if you want to stay out of debt.

The final lesson was coming to a close and I had really enjoyed my time at the school but there was just one thing I wish I had had more time to cover. I was surprised when I asked the students in the first lesson what they most wanted to learn how to save money on and their answer was 'food'. Unfortunately I had run out of time but there was one thing I could do to help them save money on food that would be more valuable than anything I could teach them in an hour long lesson. I gave them all a copy of the $21 Challenge book. You would have thought I had given them the moon! Since then, both the students and their parents have told me how much they have enjoyed the book. I'd like to think it will end up in the kitchen of their flats or dormitories when they leave home - if their parents will part with it that is!

Another thing that the students have told me is that they thought that learning about saving money was going to be boring, but found that it wasn't at all. I would love to say that was down to my general wonderfulness as a teacher but definitely not! The reason it wasn't boring was because of all the wonderful material I had to share from Simple Savings - and let's face it, the reason we all love SS is because it makes saving money easy and fun, rather than the cumbersome chore people assume it to be. I think I definitely learned as much about teaching as the students learned about saving and while I thoroughly enjoyed the experience, I think I'll leave it to the professionals from now on!

So that's one challenge down and there's another just round the corner! I just took a peek at my calendar and realised that next month is Double Dinners Month. One word - eeeek! I don't know why but I have always been rubbish at cooking in bulk. Correction Penny - be honest, you've just never had the confidence to give it a proper go, have you? *Sigh* 'tis true! Last time I thought I would be clever and make a double batch of Shepherds Pie I ended up with mince and potato soup. I guess maybe I've just never used the right recipes! However, it's a skill I would really love to have and this month is certainly a good time for me to give it a go. Ali has just been selected to represent the region at rugby, which will mean three nights a week training and a lot of time travelling. I can see dinner going decidedly pear shaped in the evenings if I don't get my bum into gear and get organised. This is one challenge I'm determined to do really well!

10. Homeopathy Corner: The Big C

It's a word we all dread. Nobody wants to receive a cancer diagnosis. Unfortunately many of us or our loved ones are affected by 'the Big C' at some time in our lives. Whilst chemotherapy and radiotherapy is a valuable and effective part of cancer treatment, the side effects can be many and unpleasant. In this helpful and informative article, Fran Sheffield explains how homeopathy is frequently used by cancer sufferers to ease the discomfort and various side effects of conventional cancer treatment. A must-read:

homeopathyplus.com.au/homeopathy-for-radiotherapy-and-chemotherapy-side-effects

11. From Last Month: Spendaholic Husband

Last month Cathy H asked:

"My husband is turning 50 this year and I am 42. I am a stay at home mum while my husband is the wage earner. Unfortunately he is a spendaholic. He cannot be bothered to inconvenience himself to save a few dollars. Catching a taxi is more convenient than a train and he will buy anything he wants without another thought. Money is tight at the moment and I am concerned as we are going heavily into debt. He is in control of the money as he earns it. I have no knowledge of exactly what he earns and where the money is distributed because he is a business owner.

"I am a great believer in 'look after the pennies and the pounds will look after themselves' but he just shrugs it off and keeps spending. He believes that one day he will 'strike it rich' and all the debts will disappear. We have four children aged from 10 years to nine months. We are locked up so tight financially that we cannot borrow a cent. He is not getting any younger and I am really scared that one day he will die and leave me with a massive debt and the costs of raising the kids. We have limited super - certainly not enough - and no other investments. Has anyone got any suggestions to try and make him change his ways?"

Thank you to everyone who wrote in with helpful suggestions for Cathy. Hopefully these will make a big difference!

Thwart spending habits with forward planning

Being prepared and organised is my way of combating my husband's spending habits! My husband doesn't want to know about money and saving, and he would rather die than use a voucher, but by being one step ahead I can help to cut back on unnecessary spending.

By anticipating what's likely to come up I can avert splurges, for example having a pizza in the freezer and wine bought on special on nights when hubby is likely to want to eat out.

Each month I prepare a 'know what you owe chart' and prioritise our debts according to interest. Having this down in black and white makes it harder to ignore and makes it easier to discuss what we owe and what it's costing us.

Knowing exactly what you owe and paying off one debt at a time makes the whole situation much clearer and takes the emotion out of it. Being prepared gives you power over your debt situation and the confidence to believe you will overcome it.

Contributed by: Nerida Stocks

Track hubby's spending to reveal true savings

If the spending habits of a family member are causing you stress or having a negative impact on you, try tracking their spending for a month to highlight the problem.

If sitting down to talk about financial problems hasn't worked, perhaps the hard facts will. By writing down everything your loved one spends, you can show them just how much that $2.00 here and $5.00 there adds up to at the end of the month, and that this money could be used more wisely.

Contributed by: Marleen Slo

Working together works out savings

I got my husband to come around to the idea of budgeting by making it something we do together.

When we first got together we were in a lot of debt but he just wouldn't adopt a saving mentality. Rather than doing all the calculations myself and telling him what he can and can't spend, I got him involved by asking him to work out things like our annual credit card interest and how much it would cost per fortnight to pay our utilities (rather than getting a big bill each quarter).

By doing this he felt he was in control of our money and involved in making our budget. He also saw the hard figures for himself so it was a good wake up call.

It seems like a small gesture, but it really helped to change his attitude. For example, his lunch was costing $50 to $100 a week which would really make me mad, but now he is in to the idea of taking lunch from home and I encourage this by making sure I cook extra each night so there are always some nice leftovers. Working together really works!

Contributed by: Wendy Caire

Pocket life's luxuries without breaking the bank

My husband and I control what we spend by allowing ourselves an agreed amount of 'pocket money' each week which can spend as we wish. After paying off the regular bills such as groceries and utilities, we give ourselves an allocated amount for things like lunch out, dinner, movies, clothes, haircuts and so on. Each person can choose how to spend their money without having to justify it to the other. It means we can each have our little luxuries (like my husband's new canoe which he bought a couple of years ago by saving up his pocket money), but because it's a set amount that we can afford, our spending on such luxuries doesn't get out of hand. In fact the opposite has happened because we have gradually reduced the allocated amount of pocket money as we have got better at saving.

Contributed by: Pippa

Owning up to debts is first step to recovery

My husband and I took control of our growing debts and now save over $1000 a month after taking a long hard look at exactly what we were spending. With credit cards almost at the limit and living month to month, the final straw came when we went into overdraft and were then charged by the bank. It was hard to do, but nine months ago we pulled out our bank and credit card statements for the previous three months and calculated just how much debt we were in. We were shocked at how much we were spending each month, but it forced us to establish a budget.

One thing that stood out was how much my husband was spending during the day - approximately $800 a month! We realised that his credit card could be cleared just by taking his own lunch and snacks to work. We also cut our grocery bill from between $300 and $500 per week to just $150 per week, and only allowed ourselves to withdraw $150 a week from our account so we could actually see our money. I quickly learned to bulk buy, scour the mailers and buy things on special.

In the last nine months we have paid off our credit cards and bought a new car, and are going on a holiday next month! We now put over $1000 per month in a high interest savings account which gives us a cushion for emergencies. It's amazing what you can achieve by facing up to your debts and digging your head out of the sand!

Contributed by: Zoe Crook

12. This Month's Help Request: Coping as a Carer

This month Bianca asks:

"Hi everyone, I am a single mum with two kids aged 13 and 9. My eldest boy has recently been diagnosed with Asperger's and he is not coping at high school. I am facing the likelihood of becoming his full time carer and undertaking distance education to get him through. Does anyone have any experiences that they would be willing to share about managing financially as a carer?"

If anyone has any suggestions or experiences which could help make things a little easier for Bianca during this time of adjustment, please send them in to us here.

13. Savings Story: $14,000 a Year Savings

I am saving $14,000 a year - thanks to Simple Savings! My partner and I (both in our twenties) were spending about $800 a fortnight on food, sometimes more. People would be astounded if they heard that and would think it's impossible but it's not. We ate out constantly and when we ate at home we would buy steak and would never make a salad without lashings of bocconcini, olives and all the other good stuff! The amount of food we threw out was phenomenal and we NEVER ate leftovers. An evening meal for the two of us cost $50 on average. I had never done a weekly or a fortnightly shop until this year. I usually went to the supermarket every night at around seven thirty when we finally worked out what we felt like for dinner. If I only paid $30 for dinner I would be extremely pleased, but I always expected the total to be around $45-$50, for just one meal!

Anyway, to cut a long story short, one day I had to go to ALDI for something and when I tried their food - I realised it was fine! While I still need to go to Coles for some things, now I buy the bulk of my groceries from ALDI. Every fortnight I write a list of what meals we would like to eat and make a mock order to see how much it is going to cost, using the Coles and ALDI websites. This worked well in itself and we were saving money but then I had another brainwave. Instead of simply clicking away at all the ingredients I wanted for the entire fortnight, I worked out how much each individual meal from our planned 'menu' was going to cost. I was absolutely gobsmacked to see that some of the meals I considered to be cheaper were actually the most expensive meals we were eating!

So now I have a list made up of all the meals we like and the price next to them, much like a restaurant menu. At the start of each fortnight my partner and I sit down together and we can choose any meals we like - provided they stay within the fortnightly budget.

This has given us much more liberty in the variety of meals we eat and it has also made us much more aware that whilst you may think nachos or burritos are cheap, it's much cheaper to make Spaghetti Bolognese!

It takes a little time to work out how much each meal costs to start with but it's well worth it. For example, if you have a recipe that uses a cup of Mozzarella cheese but you have to buy the whole bag, work out roughly how much will get used and divide up the cost. If you're serious about saving money you will do it. We have cut our fortnightly food bill down to $250, saving $550 a fortnight!

Having all our meals planned and costed in advance means you take almost the exact money to the grocery store. I take $10 more, just in case of a price change in anything but it means I no longer get sucked in to buying little extras. We have fun sitting down together and choosing our menus!

Simple Savings motivated me to take control of our finances and stop being lazy; being lazy costs a lot of money!

Contributed by: Brook Sutherland